Myth-buster opening — what people claim and what actually matters

The rumors feel inevitable and sharp: DiDi Finance buries commissions, imposes punishing interest, and traps riders and drivers alike. The truth is more measured and darker in a quieter way. Here I dismantle common myths about didi finanzas, using observable markers from Mexico City and the shift in payments during the COVID-19 pandemic as anchor points. The goal is simple: show which claims are factual, which are noise, and how to use practical tools—like no-annual-fee cards and installment plans—to reduce cost exposure without naive trust.

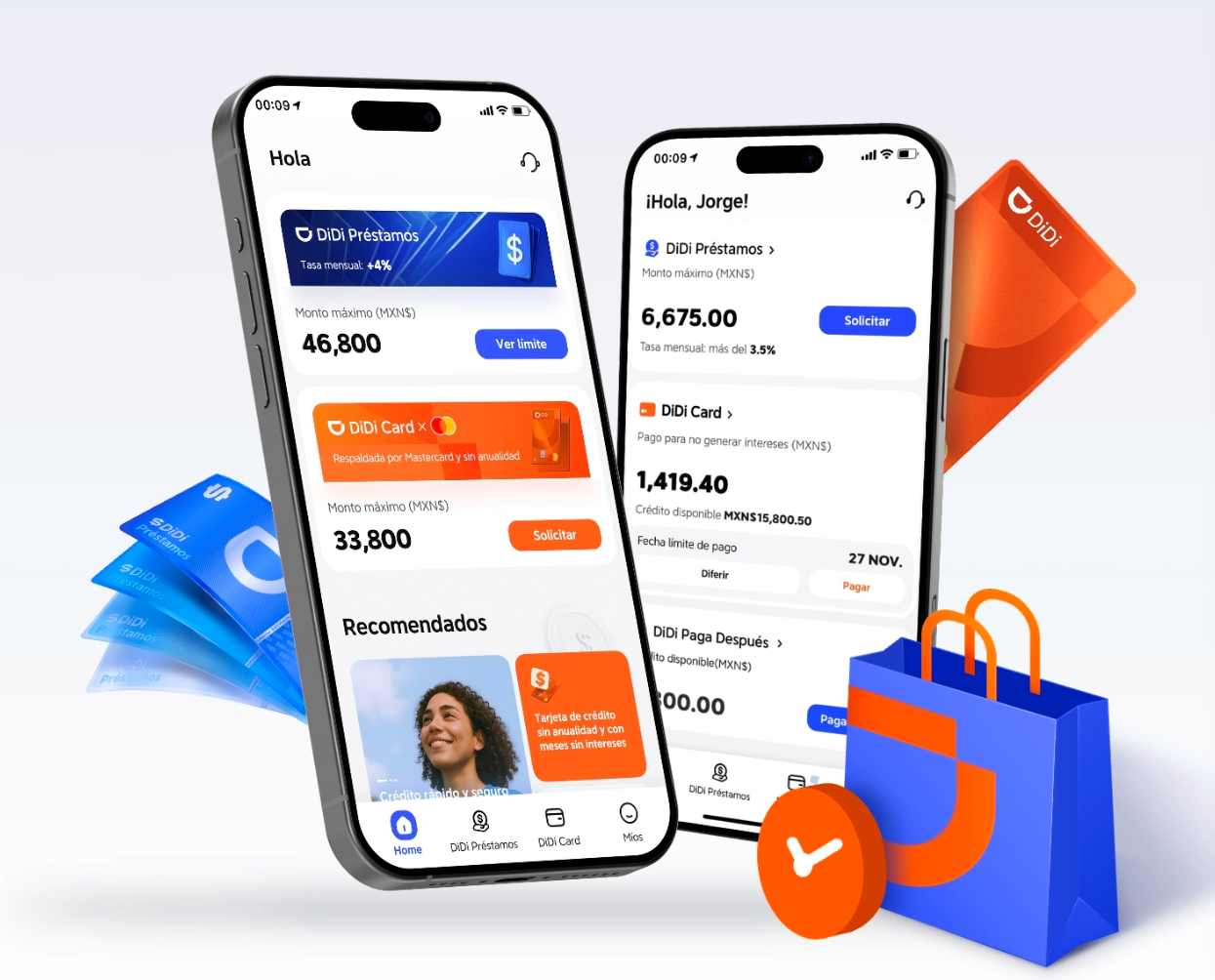

Myth 1 — “Hidden commissions everywhere”

Reality: transparent fee lines exist, but they can be missed. Platform fees and service charges are typically shown in trip breakdowns or merchant statements; the horror comes when users skip the fine print. DiDi and many fintech services separate commission, VAT where applicable, and optional insurance. That separation isn’t sinister; it’s lax reading habits that cause surprise. A few cents can stack into meaningful sums when repeated. Industry term: APR appears when balances roll into credit, not on one-off ride charges.

Myth 2 — “Interest rates will swallow you overnight”

Reality: interest rate levels are set by underwriting and product design. When a credit product converts a promotional, interest-free period into standard finance, that’s where costs become visible. Installment plans labeled “months without interest” are common; they work only when you meet payment schedules and avoid revolving balances. If you let an installment lapse, penalties and retroactive interest can apply. Track the credit limit, payment schedule, and APR to stay safe.

How to actually save: cards without annual fees and using months without interest

No-annual-fee cards and well-structured installment plans are the blunt tools that cut through small, persistent drains. Use a no-annual card for recurring platform credits and cashback categories tied to mobility or food. Pair that with clearly defined installment plans: confirm the total cost, confirm that the plan truly posts zero finance charges, and set automated payments to avoid human error. Industry terms: cashback and installment plans matter more than marketing language. Keep statements; reconcile monthly.

Common mistakes and practical corrections

People confuse promotional credits with net savings. They accept offers that require minimum spend or that expire quickly. They ignore transaction timestamps and end up paying interest by missing the grace period. — Pause and set two simple rules: auto-pay the minimum and reconcile all DiDi charges weekly. If a charge looks off, dispute it before the billing cycle closes.

Alternatives and comparative insight

Alternatives include mainstream banks’ no-annual cards, other fintech wallets, or prepaid solutions. Compare using three concrete axes: effective annual cost (including hidden service fees), flexibility of installment plans, and dispute resolution speed. Real-world anchor: drivers in Mexico City shifted rapidly to digital wallets in 2020; those who tracked fares and reconciliation fared better. This isn’t theoretical—it’s the day-to-day arithmetic of people who survive on margins.

Advisory closing — three golden rules for evaluating DiDi Finance and similar services

1) Inspect total cost, not headline offers. Add up commissions, VAT, and any deferred interest to calculate the effective cost over the expected use period. 2) Prioritize payment controls: choose cards or apps with strong auto-pay and alert features so installment plans remain truly interest-free. 3) Test dispute and refund workflows once with a small transaction; responsiveness predicts long-term reliability. These metrics give you measurable signals, not promises.

DiDi Finanzas fits into this logic as a tool—one that can either slice expenses or blur them, depending on how you treat fees, cards, and schedules. Trust the ledger, not the rumor. —